In most financial situations, the better your credit score and history, the better your options. Having no or bad credit can make it difficult to get a car, but it's not impossible. The biggest challenge is getting a loan that fits your budget. Get expert advice on how to do just that, as well as tips on how to improve your credit score along the way.

Who is This Guide for?

When you hear "bad credit," you might automatically think of maxed out credit cards or late payments. While these things do lead to bad credit, there are other situations that can cause someone to have a low credit score. If you relate to any of the following profiles, this guide can show you how to get the best possible car loan.

The young adult with no credit history

If you're a young adult, you may have never had a credit card or have only had one for a few years now. This is known as "credit invisibility". While this means you have no debt, which is great, it also means lenders have no easy way of assessing whether you can be trusted to pay back a loan. As a result, you may only be approved for a high interest rate when trying to get an auto loan or you may be required to get a co-signer.

The avid shopper with lots of debt

If you use your credit cards often, don't pay them off monthly and are sitting on a large amount of debt, that's another concern for lenders. Even using more than 20 to 30 percent of your credit can affect your score, and maxing out your cards can cause your score to plummet. Having lots of debt suggests you don't have a lot of income and need to rely on borrowed money - two things that can lead to missed payments.

The person who misses payments or has defaulted on a loan

If you've consistently missed payments or have defaulted on a loan, your credit score will drop. Lenders see these as indications you're not reliable when it comes to paying back borrowed money.

The co-signer who paid the price

Being an authorized user on someone's credit card or serving as a co-signer can be a huge risk. If the other person isn't responsible with his or her credit, it'll lower not only their credit score, but yours, too.

Why Credit Matters When Getting a Car Loan

Your credit score is one of the most important factors in determining the rate on your loan because it shows lenders - whether it's a dealership, bank, or credit union - how trustworthy you are with borrowed money. Your score will determine how much money you can borrow and at what interest rate. "Think about it this way: credit is short for 'credibility,'" said Charles Cannon, manager at a BMW dealership in Houston, TX. "It gives a lender a snapshot of your ability to pay people back in a timely manner and [whether] you are purchasing more car than you can afford."

UNDERSTANDING YOUR CREDIT SCORE

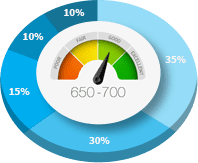

Your credit score is determined by your credit history. There are a few different types of credit scores, but by far, the most widely used is called FICO (short for Fair Isaac Corporation, the firm that invented this scoring system). According to Secrets From An Ex-Banker by Nick Clements, this is because Fannie Mae, Freddie Mac and Ginnie Mae mortgages, which represent more than 90 percent of all purchased mortgages, use the FICO score. Your FICO score is affected by the following factors:

PAYMENT HISTORY (35 PERCENT)

Do you have a history of making payments on-time, or are you usually late? Are there any delinquencies on your record, and if so, how long have they been overdue? Payment history makes up the largest chunk of your credit score. Lenders want to know you have a good record of paying back borrowed money, whether it's a loan or credit. If you've struggled to pay off debt and/or loans, it'll be reflected by a drop in your score. But the good news is you can turn things around fairly quickly — start making payments on time and your credit score will get a boost.

AMOUNT OF MONEY YOU CURRENTLY OWE (30 PERCENT)

Having a mortgage, other loans and lots of credit card debt means you probably already owe a lot of money, which can make lenders nervous. Depending how much of a monthly bite this takes out of your income, lenders may think you won't have enough money to make your car loan payment. This part of your score also reflects for how close you are to reaching your overall credit limit - the closer you are to maxing out, the lower your score.

LENGTH OF YOUR CREDIT HISTORY (15 PERCENT)

How lenders determine the age of your credit varies. Some may take the average age of your open accounts while others may look only at the age of your oldest account. Either way, all lenders are looking for proof you have experience handling borrowed money and a history of timely payments. The longer the credit history, the better the gauge for lenders. If you're getting ready to apply for an auto loan, don't open any new credit or store cards, take out a loan or close older accounts: All of these can pull down your credit score.

CREDIT MIX (10 PERCENT)

There are two types of credit on your report - installments like auto loans, mortgages or student loans that are capped at a set amount each month; and "revolving" credit such as credit cards. In the latter, the amount you owe each month depends on the amount you charge and how quickly you pay it off. Although there is no perfect mix, lenders like to see experience with both types of credit.

NEW CREDIT (10 PERCENT)

This part of your score is based on how often you've applied for loans or credit, which may be seen as a sign that you're down on your luck. Opening several new lines of credit in a short amount of time could put a dent in your score.

Source: FICO

Other Factors Lenders Look At

How much you take home each month can either help or hurt you. If you have a six-figure income and manage your money well, you'll probably have an easier time making payments than someone living on minimum wage. If you have bad credit, a fairly low debt to credit ratio combined with a high income may help you get a slightly better loan because at least lenders know you have a steady flow of money coming in each month. Conversely, if you have good credit but low income and a high debt to credit ratio, you may get charged higher than normal interest. Lenders may also look at your savings accounts to see whether you have money set aside for an emergency.

If you have a lot of payments to make each month and a high debt to income ratio - that is, you don't have a lot left over after you make the payments - it can make lenders nervous. They want to know paying back their loan is a high priority and that you won't get bogged down with other financial obligations.

Getting a new or used car can greatly affect your loan rate. Newer cars will generally have lower interest rates, whereas older, used cars tend to come with higher rates. If a newer car is repossessed, it can still be sold for quite a bit of money, making it less of a risk.

If you can make a large down payment, you won't have as much to pay off in the following months, which is ideal for a lender. If you have a low credit score, pay as much of the car upfront as you can. "Ideally, 20 percent down of what you want to purchase gives you the best chance," says Cannon.

WAYS TO BOOST YOUR CREDIT SCORE

Check your credit report for errors and dispute any you find. You're entitled by law to one free annual credit report check. Keep in mind, however, that disputes may take up to 30 days to resolve so it may be a few weeks before you actually see your score go up.

Pay your bills on time. If you're behind on bills, get caught up quickly and avoid late payments in the future by setting up automatic payment reminders or autopay.

Reduce the amount of debt you owe by paying more than just the minimum payment each month, if possible.

Don't open any new credit cards. Additional lines of credit could hurt your score and may lead lenders to believe you're short on cash.

Keep your car loan search within a two-week period. Multiple credit checks outside of a 14-day window can lower your score.

Keep balances as low as possible on any credit cards you're currently using by relying more on cash or debit as often as possible. Studies show using cash instead of cards can help you stick to a budget and spend less.

If you feel like you're drowning and can't make ends meet, see a credit counselor to help you come up with a plan.

Source: FICO

Steps to Getting an Auto Loan with Bad Credit

Remember, getting a car loan with bad credit isn't impossible, but the outcome won't be as favorable as if you had good credit. The typical steps for getting an auto loan are the same for all prospective car buyers - apply for a loan, get approved, choose your vehicle - but there are some additional steps you may need to take if you have bad credit. Here's how to get the best possible car loan with a less-than-ideal credit score:

Start improving your score by paying down debt

Danny Rosario, an auto specialist at the SCE Federal Credit Union in El Monte, CA, explains, "The debt-to-income ratio is a variable that determines how much outstanding debt you have compared to how much income you earn every single month or year, so it's important to keep these balances down." Before applying for a car loan, try to pay down your credit cards, so you don't have a high amount of debt-to-income ratio.

Compare multiple lenders

Shop around with different lenders to ensure you receive the best rate possible. Start with your personal bank or credit union. Since you already have a relationship with them, they may be more understanding about your credit history and think of you as less of a risk than other financial institutions where you have no existing relationship.

If possible, choose the loan with the shortest term

Because of your credit, your interest rate will most likely be high. Having a shorter loan means you'll have to pay more each month; however, this will also help limit the amount of interest you pay overall and will get you out of debt faster.

Consider a co-signer

This may be a requirement from the lender, depending on how bad your credit is. However, even if it isn't required, it's something you may want to consider. Co-signers are like safety nets in the eyes of lenders - they're people with good credit scores who are willing to sign a contract stating if you fail to make your car payments, they're liable. Your co-signer needs to be willing to take that risk, so make sure it's someone with whom you have a mutually trusting relationship. Young adults with no or little credit history often have parents co-sign if their parents have good credit scores.

Be open to different types of vehicles

Once you've been approved, it's time to start looking for a car, but keep an open mind. "When you have bad credit, you're likely to be limited," says Cannon. If you're getting a loan from a bank or credit union, they dictate the terms, which are likely to be strict if you have bad credit. A dealership also may not have many cars that fit within your loan terms. To avoid potential disappointment, get approved for a loan before you start test-driving so you have an idea of the types of cars actually available to you.

Where to Get a Car Loan When You Have Bad Credit

The three common lenders - banks, dealerships and credit unions - still grant loans to people with low credit, depending on their circumstances.

Making It Work with a High Interest Rate

Sometimes there's no way to get around a high interest rate when you have bad credit but you also really do need a car. When this is the case, there are a few things you can do to avoid defaulting and making your credit score worse.

Refinance your loan

When your credit score rebounds, try refinancing your loan to get a lower interest rate. Wait a significant amount of time, perhaps a year, while you boost your score, then shop around for refinancing options and crunch the numbers to see if you can lower your monthly payments.

Pay it off as soon as possible

When struggling with a high-interest car loan, it's better to pay it off ASAP to avoid paying more for the car than it's worth. If you have other payments you're working through, like credit card debt with lower interest rates, pay the minimum possible on those accounts so you can throw extra cash at your car loan.

Use your tax refund wisely

If you get a tax refund in the spring, apply that to your car payment. It's often a significant amount of money people forget they'll be receiving.

About the Author

Claire Swinarski

01/03/2022

"How to Get a Car Loan with Bad Credit"

www.moneygeek.com/auto-loans/bad-credit/